Pooches, Powell and SIMPLICITY

Are Dog Days Gone? Where are Markets in the Recession-Inverted Yield Curve Cycle? Where are YOU in YOUR investment Cycle?

Congratulations, “Bandit” (top center) Garden and Gun’s 2023 Annual Good Dog Contest winner. More honorable mention pooches to be recognized here before we go down the “Dogs of the Dow” and Yield Curve inversion data dump. Sit. Stay. Read the blog. Good Dog.

Week In Review

Impressive gains across the board from all markets this week as US markets post best weekly gains for the year this week up 5%+. US Equities, International Equities and the Bond market all posted gains as Fed Chair Powell keep rates steady and continued with the FOMC’s “pause” stance. Powell offered “The risks of doing too much vs. the risk of not doing enough are “getting closer to being in balance..” at Wednesday’s FOMC meeting.

Are the Dog Days gone? Sadly, I need to warn of potential rough seas ahead. While our proprietary “Switching” indicators are about to flash a short-term green light to reinvesting some cash from the sidelines (noting that “10 Year” money stayed invested), the bigger, opposing and more bleak picture could be told by the current inversion of the yield curve.

This inversion story has been unfolding since November 2022 and has some time to play out. Portfolio Strategy based purely on the current Inversion Cycle suggests buying 10-Year Treasuries and SELLING the S&P 500 in 2024 Q1. Scarry talk, right? And neither a trick nor a treat. With Halloween in the rearview mirror, and Thanksgiving approaching, let’s look to the light, and eat this Inversion Cycle headline one bite at a time.

For starters, Alphavest does NOT base our portfolios and strategic allocations on one or two indicators or theories, irrespective of their track records. You’ve heard me rant on how diversification and safety has not “returned” to investors in 2023, yet remain vigilant in those pursuits. We are also diverse in our many indicators and market guideposts and never rely on one to determine our path.

Next, Yield Inversion Cycle backstory: November 2022 was the 9th time the 10-year and the 3-month U.S. Treasury yields inverted since 1955–an inversion is considered when the 10-year yield is below the 3-month market yield. When this occurs, there is a near perfect track record to forecast economic and financial downturns. I’m feeling those, “run for the hills” comments from readers right now and need to remind all: COMPOUNDING and timing markets are NOT friends. Rather, it’s a complicated dance.

The Darkside:

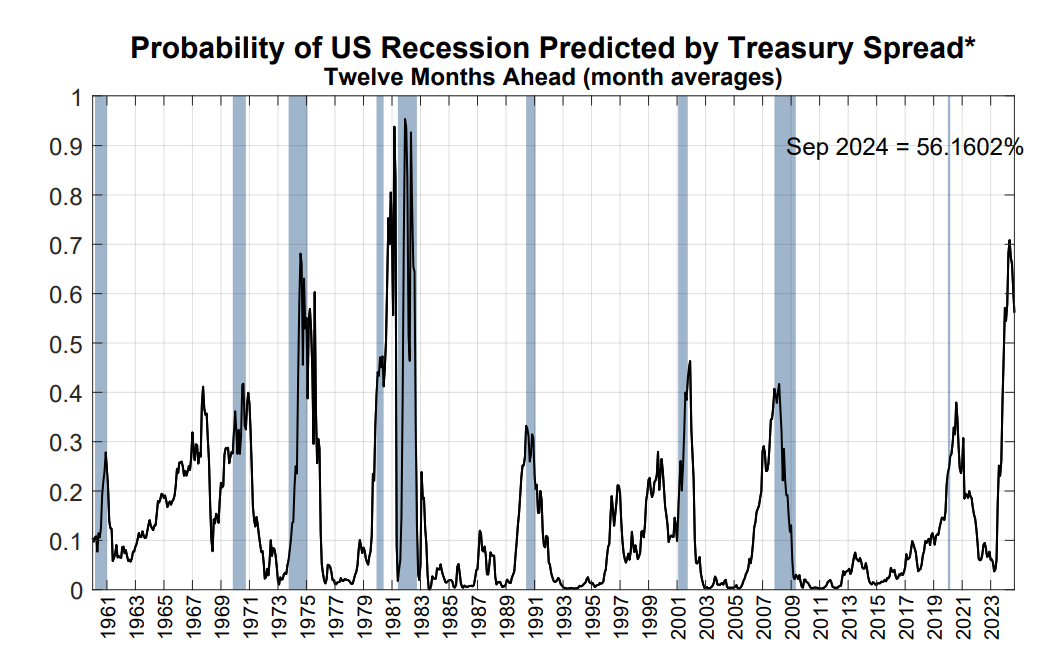

The madness of all the rate hike now starts to have a more meaningful role; If the rate hike cycle is over, one concern is that recessions almost always follow a rate hike cycle, and this cycle has been faster and larger than most. The Federal Reserve data/below points to a 56%+ likelihood of a recession:

Sources: Board of Governors of the Federal Reserve; National Bureau of Economic Research; authors’ calculations.

Notes: Parameters estimated using data from January 1959 to December 2009; recession probabilities predicted using data through July 2019. The parameter estimates are α= -0.5333, β= -0.6330. The shaded areas indicate periods designated as recessions by the National Bureau of Economic Research.

The Lighter side:

A historical timeline–the “gift” of pretty solid crystal ball, backed with strategic portfolios/indicators to side-step a meaningful market downturn, AND continued wafts of a “soft landing.”

Knowing that the last rate hike typically precedes recession by a year on average means we have time … In order to correctly position for what is, historically, most likely to happen– investors MUST understand not only where we are in the inversion/recession cycle–but also, where YOU are in YOUR investing and savings/withdrawal cycle.

A broken record come to mind? Indeed.

Yet it deserves to be repeated; having a strong sense of your allocation and investment PLAN is critical to what you do in the wake of what may begin to unfold in 2024.

AND…a soft landing is possible, as was true in 1995.

What Is a Soft Landing? A soft landing, in economics, is a cyclical slowdown in economic growth that avoids recession. A soft landing is the goal of a central bank when it seeks to raise interest rates just enough to stop an economy from overheating and experiencing high inflation, without causing a severe downturn.

Its confession time, with a dose of overwhelm AND underwhelm here for you today:

As asset managers, we–and MANY got it wrong in 2022. Our portfolios in 2022 were overly tactical and too “artsy’ with strategic commodity allocations based on commodities ruling the Asset Scale in 2022. All resulted in portfolio under-performance.

Déjà vu time? Yes and no. Commodities are BACK at the top of the asset scale…Our commodity stake is 50% less, this year, than it was in 2022, despite commodities, yet again, leading the Asset Scale. Unlike last year–and our extensive data backs this approach–tactically allocating to bonds and/or cash will not only mitigate the performance mistakes of the past, but may even come with a significant performance boost given the state of short term interest rates and bond price outlook (favorable).

I know from many life lessons that the best way to get through a ceiling of complexity is to GET SIMPLE. Our models and allocations are showing us that simple is working. Less art, more simplicity. Since moving to highly stressed tested, researched and more simple switching protocols and securities used in switching (cash and bonds vs. commodities, for example), our models and our client’s portfolio’s standard deviation, AKA overall risk, is declining while at the same time, returns are meeting benchmark standards; a combo sought after but hard to attain. Getting simple did this.

So, let’s get more simple:

Are you…

Under 50 and no plans to touch a penny until 60-ish? Go to Door #1.

55+ and looking to retire in the next 5-10 years? Go to Door #2.

Retired and actively withdrawing funds from your Portfolio/savings? Go to Door #3.

It really can be that simple.

With all the noise and recession speculation, we will stay disciplined to indicators and strategic models and allocations as we endeavor to compound, reduce risk and to keep it simple. Join me in this walk…what number door are you walking through at this phase of your investment cycle? Need a hand? Let’s decide together.

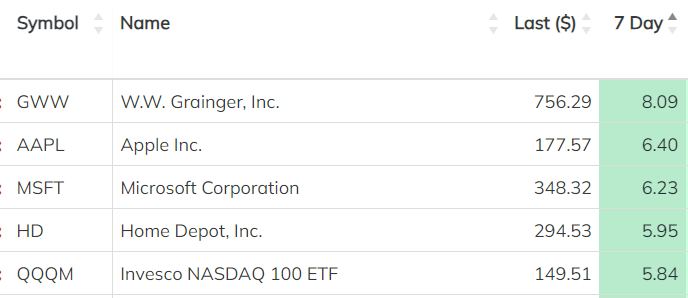

Now, for winners and losers….

Winners:

Tech for the win this week…and finally, Home Depot gets a boost.

LOSERS

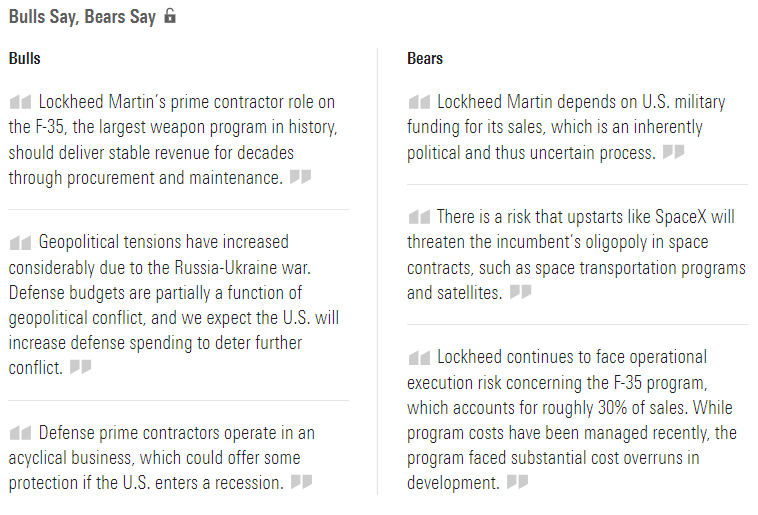

We sold Lockheed Martin/LMT from the Alphavest Equity Income Portfolio this week. With a Nasdaq/Dorsey Right rank of ZERO (0-5), I’m pleased that LMT has outperformed its benchmark index, the Dow Jones Industrial Average on a 3YR basis, and that we earned over 11% on the stock in the last 30 days. Sell discipline told us now was the time.

This is a new piece, I thought I’d share from our partners at Morningstar on LMT just so you can see what the committee is evaluating as we implement our portfolio rules;

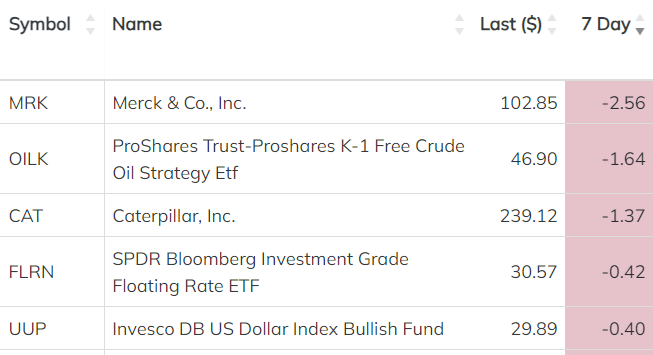

Merck at the top of the losers list this week is a strong 4 for 5’er with a dividend yield of 2.84%, that according to Morningstar, “looks secure based on a wide diversified portfolio of drugs.” MRK remains solid in the portfolio.

Be a winner and not a loser:

Join us at the office 11/15 for either our

3-6-10 Lunch and Learn 12:45 PM or

3-6-10 Happy Hour 4:30-6:30 PM

We will help you determine where you are in your investment cycle. Then, no matter what markets hold, we can SIMPLY do the rest! Can’t join us? Grab a 3-6-10 consult.

Keep it simple for more perfect days,

Advisory Services offered through

Red Triangle, LLC DBA Alphavest.

PS: Do you believe “Who Controls Capital Matters” ? I DO.

Join us for a very special Farm to Table event

3-5 PM on November 12th

Bedaw Farms, Awendaw, SC

Hear from me and TSWS Portfolio Manager, Kate Nevin

while enjoying a curated culinary experience that promises to inspire!

Subscribe to this weekly update. AND–if you enjoyed this 3 For 3,

the greatest thank you can give is a comment here or forward it to a friend. Thank you!