In the first quarter of 2015, the Standard and Poor’s 500 Index rose 0.433%, Master Limited Partnerships (MLPs) declined 5.228%, and the ten year US treasury yield declined from 2.13% to 1.93%.

The stock market has been struggling with slowing earnings, mixed economic reports and the prospect of Federal Reserve tightening.

Meanwhile, the Master Limited Partnership (MLP) market has been under considerable pressure due to the 56% decline in oil prices and uncertainty surrounding how this will impact their business prospects. With that said, we believe this is a good time to add to or increase MLP exposure.

Why?

Nobel Prize winner Robert Shiller’s Cyclically Adjusted Price Earnings Ratio is 27, signaling the market is near peak valuation levels.

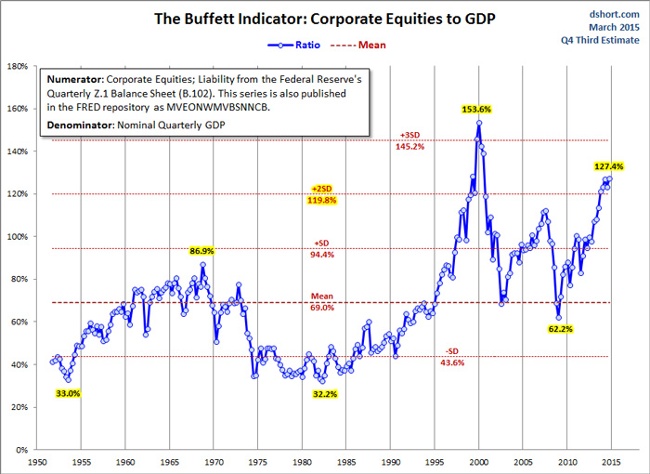

In addition, the Market Capitalization to Gross Domestic Product ratio (a so-called Buffett favorite indicator) is also near historically high levels.

Margin levels, too, are near historically high levels, suggesting the market is at risk. (However, this was true last year as well!)

Buffett-Indicator

What’s different this time, is the unprecedented level of accommodation by the Federal Reserve and other central banks around the globe which, over the last six years, has kept this tepid economic recovery on track.

It’s this unprecedented accommodation that’s led to current high valuation levels. Investors are confounded by the perplexing decision of where and how to invest when interest rates are so low, that yields are negative in some markets.

These low interest rates create a potential market risk that could lead to a correction or crash when the Federal Reserve begins hiking rates later this year. Modern banking and finance have allowed for massive international fund flows, leverage and derivatives which can create the potential for structural stresses and dislocations below the surface.

Bottom Line: Why invest in Master Limited Partnerships?

We believe this is a good time to add to this attractive income producing asset class.

What makes us particularly bullish on the MLP sector is their high tax-advantaged yields and stable businesses. MLPs currently yield 6.2%, which is over three times the yield of the ten year US Treasury note. More importantly, this tax-advantaged yield has historically grown around 10% annually, though we now forecast it to grow at closer to 7% annually in the future.

In this yield-starved market, we believe that MLPs offer attractive yields and greater price stability than stocks. Consequently, they should be overweighted, particularly in light of their recent price weakness.

From an operating and business perspective, MLPs are tax-advantaged utilities which enjoy natural monopoly status, since the Federal Energy Regulatory Commission regulates their build-out nationwide.

While the decline in oil prices has shrunk drilling rig counts and production may moderate, infrastructure supplier prices are dropping as there’s now slack in a market that had been growing rapidly.

Lastly, the United States – which has emerged as one of the world’s leading hydrocarbon producers along with Saudi Arabia and Russia – now stands out as an especially stable producer in this increasingly war-torn world.

Guest Alphavest blogger, Tyson Halsey, CFA of Income Growth Advisors, LLC, manages multiple strategies including a MLP and a Dividend Growth portfolio. The views and opinions expressed herein are that of the author and not intended as buy or sell recommendations. All data and information herein is accepted as true and accurate but has not been verified for accuracy.

Halsey brings 30 years investment experience, 14 years Master Limited Partnership investment experience, and nearly a decade of quantitative investment strategy to Income Growth Advisors, LLC (IGA).

Halsey utilizes his research analysis and investment experience to manage portfolios at IGA. He has worked at leading investment firms Merrill Lynch, Alex Brown and Deutsche Bank in the 1990s as a financial consultant and institutional broker. Halsey has worked with high net worth corporate executives in Silicon Valley and New York, and worked in the Corporate Executive Services Group at Deutsche Bank Alex. Brown.