|

September greets us with more than the crispness of fall—it arrives with clarity in the financial landscape. The markets have steadied after their wild summer run, and new policy shifts bring opportunities (and deadlines) we cannot ignore.

Most notably, the One Big Beautiful Bill/OBBB provides meaningful—but temporary—tax relief for retirees, a chance to optimize your income and withdrawals while the window is open.

At the same time, Friday’s jobs report was sobering: the U.S. economy added just 22,000 jobs in August, well below expectations, and the unemployment rate ticked up to 4.3%, the highest in years. This weaker labor market has fueled speculation that the Federal Reserve will cut rates as early as this month, with futures markets now pricing in an 88% probability of a reduction. For retirees, this means decisions about fixed income and cash yields may need to be made sooner rather than later.

This month’s 3-for-3 explores three essentials:

Policy wins (OBBB tax relief), policy pivots (rate cuts ahead), and a chance to align wealth with life’s most meaningful moments. The tools are in place—the choice is how you use them. Let’s do this!

|

|

|

|

|

|

3 For 3:

1. “$6,000 Senior Deduction Lands—Are You Maximizing Yours?”

One of the headline wins in the One Big Beautiful Bill (OBBB) is a new $6,000 standard deduction for those 65 and older—$12,000 for married couples filing jointly. Combined with the regular standard deduction ($29,200 for joint filers in 2025), a married couple can now shield up to $41,200 of income from federal tax. That’s a meaningful buffer, especially for retirees living primarily on Social Security and modest retirement withdrawals.

According to Social Security data, about 50% of beneficiaries pay some federal tax on their benefits. Under the OBBB, the number of retirees with taxable Social Security could drop from 64% to just 12%—a sweeping change. Kiplinger estimates that nearly 88% of retirees will now owe little to no federal tax on their Social Security income.

But here’s the catch: this benefit is temporary, expiring in 2028 unless renewed. That gives retirees a 3-year planning window.

Action items for retirees:

- Withdrawal sequencing: Draw more aggressively from IRAs while income is shielded, potentially reducing future Required Minimum Distributions (RMDs).

- Roth conversions: Convert at lower effective tax rates while you can, locking in tax-free income later.

- Charitable giving: Pair the deduction with Qualified Charitable Distributions (QCDs) from IRAs to maximize tax efficiency.

The OBBB deduction is more than a line on a tax form—it’s a limited-time gift. Use these years to reshape how you draw down assets and keep more of what you’ve earned.

Read more → Retirees: Here’s How to Take Advantage of New Tax Breaks

Grab a 1:1 and get clear on how the OBBB can work for you.

Did you know that some of our best 3 for 3 topics come from meaningful discussions with clients? Thank you KK for bringing this 3 for 3 to light. Partner with us! See how engagement can bring big benefits with Alphavest Partner Points!

|

|

|

|

|

|

2. “Rate-Cut Roulette: What Jackson Hole Means for Retirees”

This year’s Jackson Hole Symposium was one of the most closely watched in a decade. With inflation moderating—August CPI at 2.5% year-over-year, the lowest since 2021—markets are betting the Federal Reserve may cut rates as soon as September. Futures markets put the odds of a September rate cut at 72%, with at least two more cuts expected by mid-2026.

For retirees, falling rates bring a double-edged sword:

- Cash and savings yields: Many retirees have enjoyed 5%+ yields on CDs and money markets. A rate cut could drop those yields back toward 3–4% within a year.

- Bond prices: As rates fall, existing bond values rise. Vanguard estimates that a 1% drop in the 10-year Treasury yield could push bond prices up 8–10%, depending on maturity.

- Mortgage & borrowing costs: While fewer retirees carry mortgages, those with HELOCs or family assistance loans could benefit from lower borrowing rates.

The Fed’s dilemma is clear: ease too quickly and risk reigniting inflation; hold too long and risk a slowdown. For retirees, the key is positioning.

Action items for retirees:

- Lock in yields: If you haven’t already, consider laddering CDs or Treasuries now to preserve higher yields before cuts.

- Bond rebalancing: Slightly extending duration in bond portfolios could provide upside as rates fall.

- Liquidity check: Rate cuts may spur volatility in equities—having 1–2 years of income in cash reserves cushions against market swings.

Jackson Hole didn’t provide all the answers, but it made one thing clear: we are nearing a new phase in monetary policy. Retirees who act now can capture today’s higher yields while preparing for tomorrow’s shifts.

Read more → 3 Reasons Jackson Hole Matters This Year

|

|

|

|

|

|

3. “The Perfect Day Portfolio: Wealth for Living, Not Just Legacy”

Markets and policies will always swing—but the most profound question in retirement is this: How do you use your wealth to shape your best days, today?

The Perfect Day Portfolio is a philosophy as much as an allocation strategy. At its heart: balance. A portfolio that is neither overly aggressive (risking painful drawdowns) nor overly conservative (risking erosion by inflation). Instead, it seeks to:

- Provide growth to sustain multi-decade retirements.

- Offer safety to meet near-term income needs.

- Free up surplus to fund meaningful experiences.

Here’s where the numbers matter. The average 65-year-old today can expect to live another 18–20 years (SSA data), meaning retirement can last as long as a career. Yet studies show retirees often underspend by 20–30% out of fear of running out of money (Morningstar, 2024). In other words: wealth that could have been spent on experiences ends up left behind.

The Perfect Day approach flips that script. By allocating intentionally and using excess returns, retirees can:

- Travel with purpose: A $10,000 “harvest” from portfolio gains might fund two international trips—creating memories no account balance can match.

- Deepen relationships: Investing in family gatherings, milestone celebrations, or even helping adult children with housing creates lasting impact.

- Practice “living philanthropy”: Giving while alive lets you see and feel the difference your generosity makes.

Financial planning isn’t just about estate transfers; it’s about designing a life you love now. The Perfect Day Portfolio ensures you’re not merely preserving wealth—you’re using it to enrich your days. Been through Perfect Day Planning Process? What was your biggest A-HA?

Want a refresher or an opportunity to experience “Perfect Day?”–Grab a consult!

|

|

|

|

|

|

|

|

|

Winners and Losers

|

|

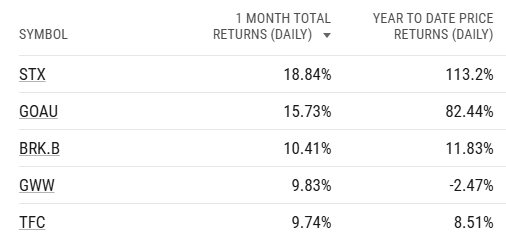

MTD and YTD Portfolio Winners

|

|

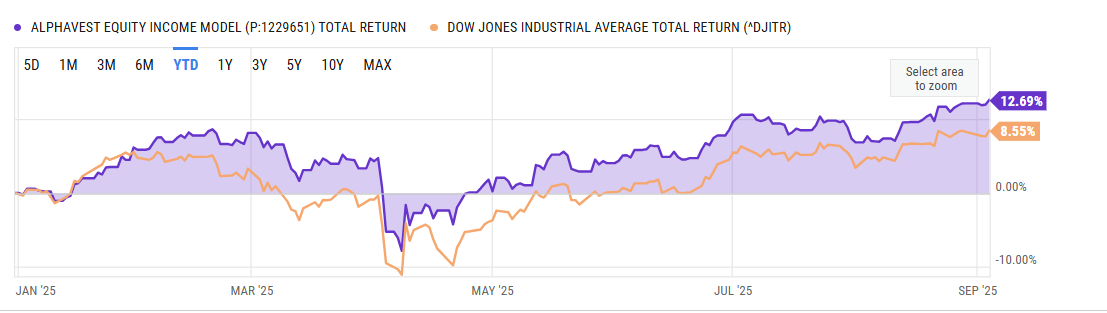

Gold play, GOAU and dividend hefty tech play, Seagate/STX are both on this month’s MTD and YTD winner boards. STX, with a 1.63% dividend yield was a new add to the Alphavest Equity Income Portfolio, replacing Eli Lily/LLY in May–since replacement, LLY is -1.14% and STX up +91.05% (not a typo and certainly a first for AV Equity Income Portfolio for a 4 month return!). AV Equity Income boasting a yield of 2.35% is outpacing benchmark index, the Dow Jones Industrial Average/DJIA, up +12.69% vs. DJIA +8.55% YTD. Thte DJIA yield is 1.46%.

|

|

|

|

|

|

|

|

|

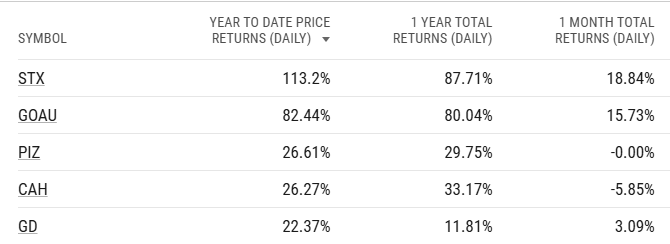

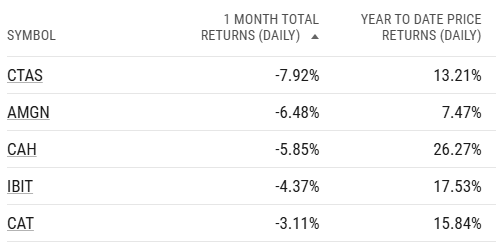

MTD and YTD Portfolio “Losers”:

|

|

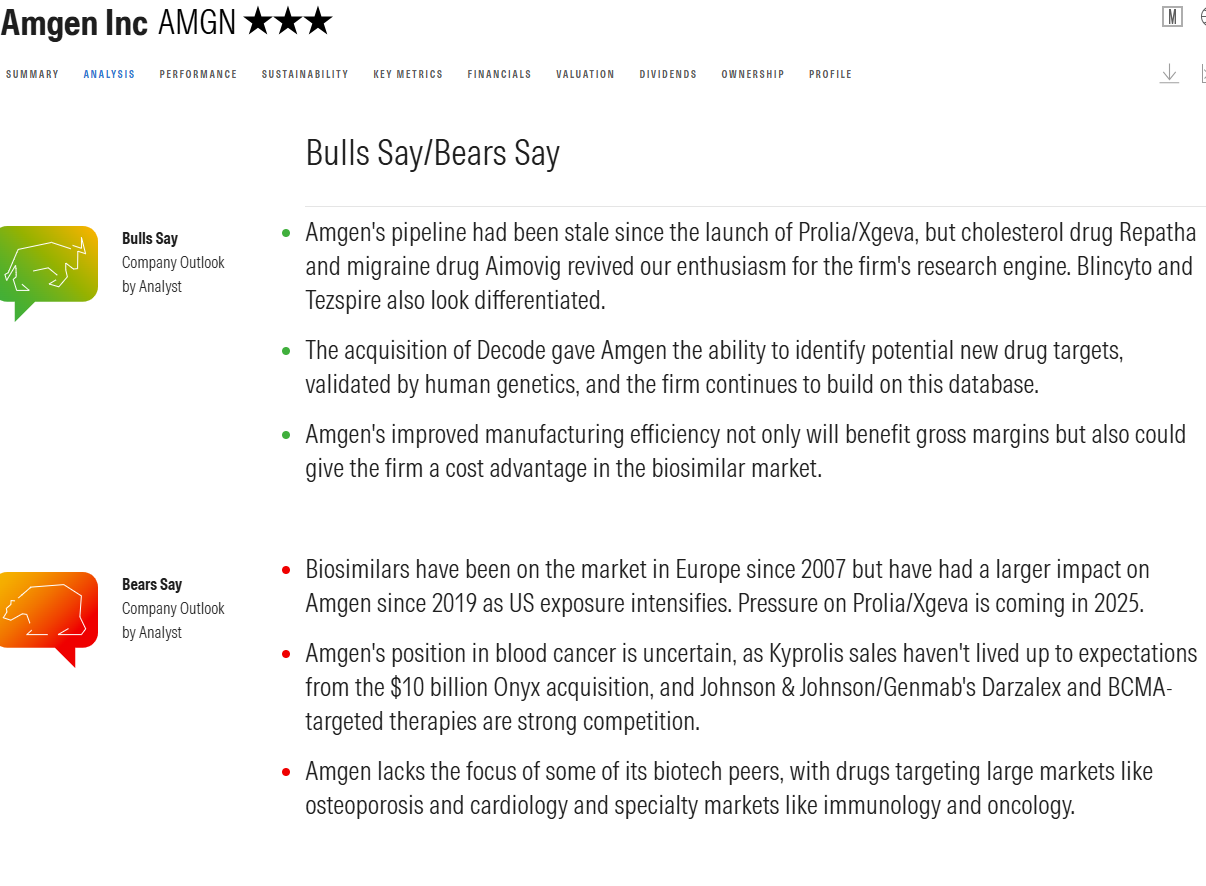

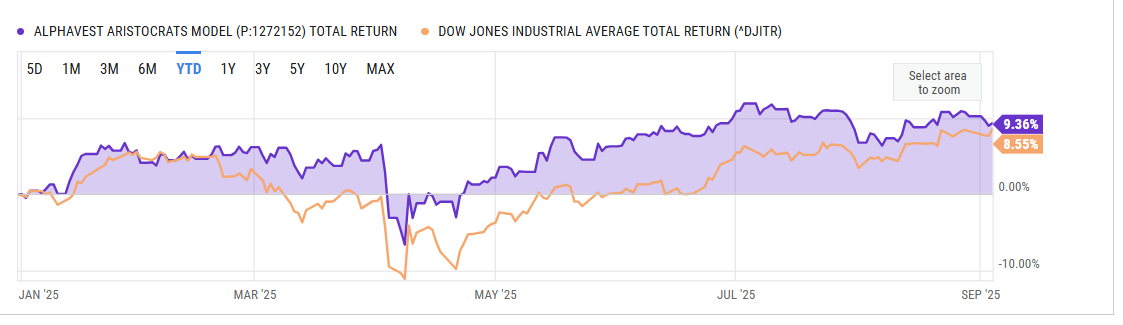

The monthly losers, while disappointing, the silver lining is that all but 1 are above the S&P 500 YTD return of +10.76% (AMGN, the exception +7.47% YTD–not too gloomy). The loser board has no positions both with MTD and YTD losses, unlike the winner board, above (this is optimal). Cancer biotech holding, AMGN is an 8% holding in the Alphavest Aristocrats Portfolio +9.36% vs. DJIA +8.55%, YTD, and it’s underperformance is not hindering the Aristocrats Portfolio from outpacing its benchmark/DJIA, YTD. With a 3.4% dividend yield and a 3 Star Morningstar rating, AMGN remains a hold.

|

|

|

|

|

|

|

|

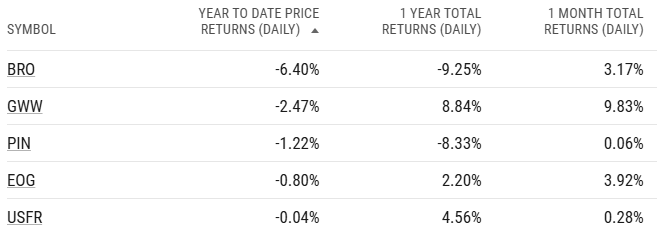

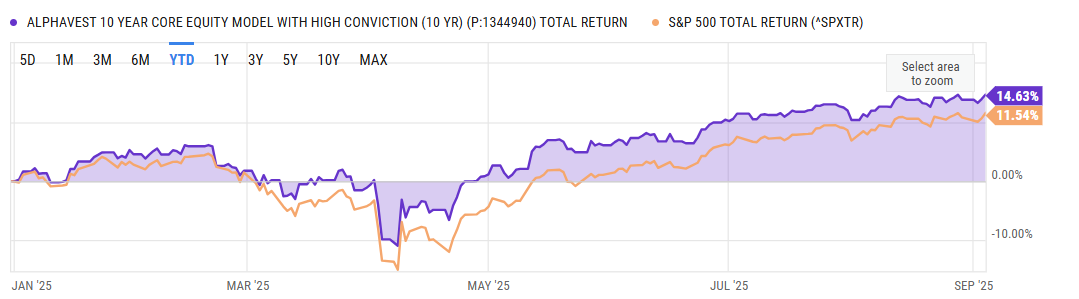

Of our YTD losers, long time holding, Brown & Brown/BRO, and International holding, Invesco India ETF/PIN are being evaluated for portfolio elimination. PIN has come underperformed with recent tarriff pressures. PIN, is a 7% holding in the Alphavest 10 YR Portfolio. PIN’s underperformance has not hindered the Portfolio in outpacing the S&P 500 YTD up +14.63% vs. +11.64% YTD for the S&P 500. BRO is an 8% holding in the Alphavest Aristocrats Portfolio +9.36% vs. DJIA +8.55%, again, YTD underperformance is not hindering the Aristocrats Portfolio from outpacing its benchmark/DJIA.

|

|

|

|

|

|

|

|

|

|

|

Events! JOIN US

|

|

|

Events on Deck:

RSVP & Bring a guest!

Lunch and Learn with Cokie

September 25th, 2025

11:30-1 PM

Location: Alphavest Office and via ZOOM

75 Port City Landing, Suite 110

Mount Pleasant, SC 29464

SAVE THE DATE!

Oysters, Clays, and Market Plays

October 26, 2025

1-5 PM

Location: Back Barn at Bedaw Farms

5282 Bedaw Farm Drive

Awendaw, SC 29429

SAVE THE DATE!

Annual It’s a WRAP! Party

Thursday, December 11, 2025

DROP IN and bring a gift or two for us to wrap! You know the gig!

4-7 PM

Location: Alphavest Office

75 Port City Landing, Suite 110

Mount Pleasant, SC 29464

|

|

|

|

|