WEEKLY UPDATE – OCTOBER 3, 2016

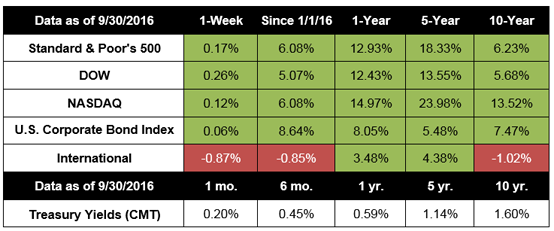

Though the final week of the third quarter ended positively for the major indexes, stocks took a rocky path to get there. A presidential debate, surging oil prices, and concerns about a global bank all took their toll on the market last week. For the week, the S&P 500 gained 0.17%, the Dow grew 0.26%, the NASDAQ edged up 0.12%, but the MSCI EAFE lost 0.87%.[1]

Why did Deutsche Bank affect markets?

Last week, concerns about one of the world’s largest banks caused investors to worry that a new “Lehman moment” might spark a new financial crisis. Germany’s scandal-prone banking giant is facing financial penalties in the U.S. for the role it played in the financial crisis; the bank’s problems are causing key clients to distance themselves and analysts wonder about the firm’s financial health. Investors reacted to Deutsche Bank’s woes negatively, setting off a 200-point drop in the Dow Jones Industrial Average on Thursday.[2]

A similar loss of confidence in Lehman Brothers in 2008 caused counterparties (major clients) to ask the cash-strapped firm for their money back, triggering its collapse and the beginning of the financial crisis. However, Deutsche Bank is not Lehman, and the world is a different place than it was in late 2008. International financial institutions are not as dangerously interconnected as they were then, and global regulators are much better positioned to respond to situations that arise.

Markets agreed with that assessment and rebounded on Friday. While news from Deutsche Bank may still create headlines, we think the worst has passed. If you have any questions about Deutsche Bank or other financial firms, please reach out to us so we can respond to your concerns.

What does the data say about the economy in the third quarter?

With the third quarter officially in the rearview mirror, analysts are turning their attention to the data. Here’s what we know so far:

The third estimate of second-quarter economic growth showed that Gross Domestic Product (GDP) grew a stronger-than-expected 1.4%, up from initial estimates. Even better, some economists think the economy could have accelerated and grown 2.8% in the third quarter, which would put it closer to the pace we want to see.[3] The latest September data on consumer sentiment, an important indicator of future consumer spending, shows that Americans are more confident in their financial prospects, possibly opening the door to higher spending in the critical holiday shopping season.[4]

What might the final months of the year bring?

As we enter the final three months of 2016, markets are contending with some headwinds we’re watching. We can expect plenty of headlines around the presidential election as we get closer to November. Political beliefs aside, elections represent a lot of uncertainty, especially with wild-card candidates. Markets may react with relief after election uncertainty resolves; however, concerns about the changes a new administration will bring may also trigger further volatility.

Britain’s prime minister announced her intention to begin negotiating the UK’s Brexit from the European Union next spring. By 2019, Britain could be a sovereign nation once again, bringing a slew of changes to the EU.[5] Though we don’t expect to see too much volatility around the Brexit until next year, it is a political football that could roil markets.

Oil prices might have finally hit bottom and be poised to rally this fall. Major oil producers, including Saudi Arabia and Iran, seem ready to coordinate production to bring oil prices back up. If a pact is made (and held), oil could head back toward $60/barrel next year, which would bring relief to beleaguered U.S. energy companies.[6] However, higher oil process could bite consumers by making gas more expensive at the pump. It’s likely that oil prices will play a role in market movements in the weeks to come.

The week ahead is packed with data, including the September jobs report, which may factor into future Federal Reserve interest rate decisions. As always, we’ll keep you updated.

ECONOMIC CALENDAR:

Monday: Motor Vehicle Sales, PMI Manufacturing Index, ISM Manufacturing Index, Construction Spending

Wednesday: ADP Employment Report, International Trade, Factory Orders, ISM Non-Manufacturing Index, EIA Petroleum Status Report

Thursday: Jobless Claims

Friday: Employment Situation

Notes: All index returns exclude reinvested dividends, and the 5-year and 10-year returns are annualized. Sources: Yahoo! Finance, S&P Dow Jones Indices, and Treasury.gov. International performance is represented by the MSCI EAFE Index. Corporate bond performance is represented by the SPUSCIG. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly.

HEADLINES:

New home sales tumble in August. Sales of newly constructed homes fell 7.6% in August after surging in July to the highest level in nearly nine years. The retreat isn’t unexpected and further volatility in the housing sector may occur.[7]

Durable goods orders slip. U.S. factories saw fewer orders in August for long-lasting goods like aircraft, appliances, and electronics. However, a core category that represents business investment grew for the third straight month.[8]

Weekly jobless claims edge higher. The number of Americans filing new claims for unemployment benefits rose slightly last week but held at stable levels, supporting the view that the labor market continues to improve.[9]

Pending home sales drop. The number of homes under contract slumped in August, suggesting that home sales fell across the board. Since pending sales forecast future activity, it’s likely the drop in housing activity will be felt in the weeks ahead.[10]