Quiet the Noise (Listen to the Data)

Below you will find a “temperature reading” on the market and the risk level on the “field.”

Relative Strength Line Up of the Asset Classes:

Q2 2015 Update: On 4/15 International Equities took back its #2 Spot dethroning Fixed Income after a brief 4 months in the #2 spot.

7/1//2015:

- #1 Asset Class: Domestic Equities

- #2 Asset Class: International Equities

- Market Status: BULL

- NYSE Bullish Percent: 51.74%% (DOWN from 60% Q2) DEFENSE (Reversed DOWN from Offense on 6/9/2015 @ 55.14%)

MLP Update: Buy low. Buy value. Buy panic. Buy MLPs.

By: Tyson Halsey, CFA

Income Growth Advisors, LLC

Income Growth Advisors, LLC has continued to deliver solid returns for its clients even though the Alerian MLP Total Return Index is down 19.81% over the trailing twelve months. This rare negative performance is primarily due to the historic correction in oil prices which began late last June. Brent crude oil prices appear to have stabilized and are trading 45% below their peak. This was the third worst decline in crude oil history and led to a sharp decline in capital spending in the oil industry and in the growth of the US shale boom. Additionally, MLPs have also been hampered by rising rates. Since yields on the 10 year US Treasury have risen from 1.6% to 2.40%, income generating assets have lost some of their appeal, and this too has been a headwind for MLPs. Lastly, the technical default by Greece led to global market weakness in recent days which explains why June was a particularly bad month.

MLPs offer an excellent value. Underlying trends in the US shale boom are improving and MLPs’ 6.5% tax advantaged yields are compelling. Though yields have increased and the Federal Reserve will continue to taper its unprecedented accommodation policy, we believe most of that damage is priced into MLPs.

Three basic investment rules now apply to MLPs: Buy low. Buy value. Buy panic.

- Since the beginning of the year, the yield on the 10 year US Treasury has backed up from 1.6% to nearly 2.5%. While the market anticipates higher yields as the Federal Reserve reduces its unprecedented accommodation, we believe much of the interest rate correction in the MLP sector has occurred and that a slow gradual rise in rates will occur over the next three years with nominal negative impact to MLPs.

- MLPs still offer a very attractive tax advantaged income offering. The index currently yields 6.5%.

- Relative to the 10 year benchmark MLPs trade at a high spread. Currently the MLP index yields 414 basis points over the US Treasury. Historically, when investors have bought MLPs at 400 BPs over the US Treasury, they have been rewarded.

- As the domestic energy sector adjusts to the lower oil and gas prices, we expect a resumption in growth and confidence in the US shale renaissance. With that resumption of growth, the MLP sector should enjoy solid price appreciation as spreads normalize and higher distribution growth prospects are again priced into MLP valuations.

- Following last year’s historic decline in oil prices, MLPs declined due to the direct and indirect influence of the commodity’s price decline on the sector.

- Natural gas prices are under great pressure which historically is when a commodity sector bottoms.

We believe the worst in commodity price behavior is behind us and that much of the impact of higher rates is priced into the MLP market. From these levels, we would expect low double digit returns for investors in MLPs driven by a growing tax advantaged yield of 6.5% and distribution growth in the 4-7% range for the next few years. Relative to other asset classes, we believe that MLPs offer one of the most attractive investment options for investors seeking stable growing income for retirement and financial stability.

*The above includes previously copyrighted material reprinted with permission.

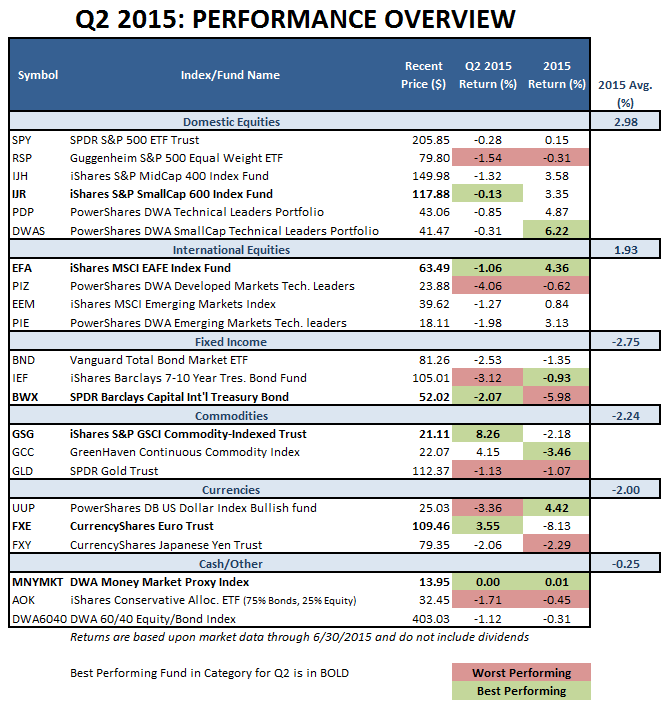

2015/YTD Market Stats

Over the next couple of reports, we’ll spend some time reviewing what took place last quarter as well as the first six months of the year, while providing insight into where we stand moving into Q3 2015. Today, we wanted to provide a quick performance overview summary. The US Equity market’s positive run ended last quarter but it wasn’t enough to move the 2015 returns into the red this year, so the market is still in the black for the year. The SPDR S&P 500 ETF SPY fell -0.28% last quarter, yet it is still up 0.15% for the year. All of the other major US Equity ETFs were down last quarter, and they have still managed to keep their positive returns for the year, most of which are better than the other asset classes. The average performance of the domestic equity proxies shown in the table below was +2.98 thru the first six months of the year.

The next best asset class in 2015 has been International Equities. The average International ETF proxy is up 1.93, roughly 1% below the average US Equity performance. Year to date, both Emerging Markets and Developed Markets have offered opportunities, but Developed Markets have taken the winners medal, as the iShares MSCI EAFE Index Fund EFA is up 4.36%, compared to the iShares MSCI Emerging Index EEM, which his up 0.84%. These areas were not immune to the underperformance last quarter, as all of the International proxies were in the red during Q2 2015.

Most of the major Fixed Income, Commodities and Foreign Currency proxies were in negative last quarter as well as for the year.

YTD Performance: 12/31/2014 – 6/30/2015

The returns for indexes, ETFs, futures, and stocks do not reflect dividends and are based on the last sale for the date requested. Returns for mutual funds do account for distributions. Performance data does not include all transaction costs. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

The Good, the Bad and The Not-so-Ugly, UPDATE

Looking back to our January 2015 Market Outlook piece “The good, the bad and the not so ugly” I thought you may appreciate a rolling market update by way of what we got right, and maybe not so right:

The Good:

The Outlook:

-

A strong Fed leadership to maintain low interest rates and low inflation

What did we have to say? …No rate hikes until the second half of the year—and that,”rate hikes should not be feared with the strong Fed leadership that’s committed to gentle changes in the name of stable US markets.” So far, STILL RIGHT.

-

Domestic Equities still occupy the #1 spot for top performing assets

What did we have to say? “Stocks maintaining a strong hold on the #1 spot is good for future growth prospects of US markets. Next year, and early on, will prove difficult for those who have benefited from buy-and-hold or point-and-shoot investment management — the market returns will come from less stocks and fewer sectors, and will also require a disciplined, focused and narrow approach in order to have a winning portfolio. Volatility will be alive and well, and the selective investor will outperform those in a Vanguard S&P 500 index fund.” STILL RIGHT.

-

A strong and growing GDP

What did we have to say? “It’s not a far reach to expect lower oil prices to give rise to consumer spending, which should help boost revenues for stores, restaurants, hotels, and more.” RIGHT.

According to Kiplinger’s and the US Commerce Dept, look for the U.S. gross domestic product to show a healthy gain of about 3% for the second quarter when the government reports the quarterly results on July 30.

The second-quarter rebound from the weather-related decline in GDP during the first quarter, along with our expectation for 3% to 3.5% growth in each of the final two quarters of the year, will put GDP growth for 2015 at 2.5%, a tick above last year’s 2.4% pace.

The biggest drag on U.S. growth going forward? Exports, which will continue to be hampered by the strong U.S. dollar, which makes U.S. goods and services pricier and less competitive in foreign markets.

The Bad:

The Outlook: A less bullish Asset Class lineup

What did we have to say? “Having both of the asset classes that are equity asset classes, Domestic and International Equities in the #1 and #2 spots is the most bullish lineup on the relative strength asset scale. And since this is no longer true, it seems that overall returns have a less bullish outlook, as well. No Longer True: As noted in the first section of this newsletter, International Equities reclaimed their #2 spot on the line-up April 15th.

The Not-So-Ugly:

The Outlook: China, not as gloomy as economists think

What did we have to say? We dispelled the many fearful sound bytes about China and the fear of it slowing worldwide economies as its slowdown ensues. With China’s GDP growth slowing, yes slowing to over 7% (wouldn’t we be so lucky!) in Q1 2015 compared to 7.3% Q4 2014 not only are other economies expanding, but the slowdown is not yet significant. RIGHT.

According to Bloomberg Markets;

“Gross domestic product rose 7 percent in the three months through June from a year earlier, the National Bureau of Statistics said Wednesday, unchanged from the first quarter and beating economists’ estimates for 6.8 percent. Industrial output in June rose 6.8 percent, while fixed-asset investment increased 11.4 percent in the first half.

The result buoys prospects for Premier Li Keqiang’s 2015 growth target of about 7 percent and the outlook for the world economy, with China stabilizing and the U.S. forecast to accelerate. Much like last year, a sluggish start spurred more stimulus as the government orchestrated a debt swap for provinces and the central bank accelerated monetary easing.”

Portfolio Changes

The biggest portfolio lag of my 19 years managing investments occurred this past 12 months. Yes, I am sharing this tid-bit of investor information—we pride ourselves on full transparency and want all of our investors to know what is and is NOT working with our portfolios. This is what Liberated Investors demand and deserve.

In December of 2014 I noticed our Long/Short was negatively impacting portfolio returns. Mid June 2015, after 6 months of due diligence and the help of an outside consultant, we made the painful, yet appropriate decision to eliminate the Long/Short Model from our investment line-up.

Many of you have been patient with the relative strength versus the buy-the-market methodology--buying the market being the strategy to which we do NOT subscribe to—and in time, with the elimination of the underperfomance role that Long/Short has played, you will see why sticking with our relative strength methodology is the best way to earn your portfolio returns.

Please contact us with your questions and to schedule a review of your performance, today.

Resources, Resources, Resources!

Check out our new website and our Resources page on the Alphavest website and explore the many resources with which we are trying to empower all investors.

A snapshot of what’s there:

Morningstar™ Fee Analysis. Learn just how much you pay each year in fees and help others to educate themselves on what they pay too! Did you know that excessive fees can amount to upwards of 21% of your wealth over a 20-30 year period? We are committed to offering the lowest fees possible and want all of our clients to know what they are paying.

Free Consultations with Cokie. Those who have used this offer have found it beneficial and have been pleased with value of 15 minutes of their time. We use this resource to offer investors a no-pressure opportunity to assess whether or not Alphavest is a good-fit. This is a great place to send those that you think may need our services. Thank you for your referrals and consideration!

FINRA Advisor Background check. FINRA reports that only only a small percentage of investors check their advisors record before making a switch. We run background checks on our employees, our childcare providers—why not run one–its FREE–on the person who manages your money? Rest assured our record is spotless (click here for Cokie’s U4). The important feature of the report is that it will report “NO DISCLOSURES,” which means no fraud or investor complaints.

Rules Quarterly

Due to the lengthy nature of this quarter’s newsletter, we have opted to skip “Rules Quarterly” this quarter.

If you really want one of my unofficial rules, however, how about this one:

Buy low and sell high—AND let an advisor do it for you. 🙂

Stay tuned…

Subscribe to Cokie’s Blog for more frequent updates on Markets and Matters….

Most of my blogs are less than 200 words – short and sweet! I have 2 weekly posts — one is uber-short and the other highlights our Investment Management “Rules” with one Rule detailed each week.

Q2 Most Read Blogs:

- What can investors learn from Coach K and the Blue Devil champs?

- Mid Quarter Alert: International Equities are back in the saddle

- Sell In May and Go Away?

Join the Liberated Investor Movement TODAY!

We launched the Liberated Investor Movement in an effort to educate investors on how to break free from being held hostage by “Big Brokerage.”

The Liberated Investor Tool Kit exposes five areas of the investment management industry where the deck is stacked against investors and offers simple and direct advice:

- Excessive Fees and What Can Be Done About Them

- The Myth of Buy and Hold

- The Emotion Behind Market Timing

- Industry Conflicts of Interest

- How to Hire An Advisor That’s On Your Side

Download the Tool Kit today and share with your Facebook community and friends and family!

The best way to refer us? Tell others to download the FREE The Liberated Investor Tool Kit:

1 http://finance.yahoo.com

2 Analysis of Bureau of Labor Statistics Data January 2015-June 2015 https://research.stlouisfed.org/fred2/series/PAYEMS/#

3 http://www.foxbusiness.com/markets/2015/07/03/smaller-workforce-more-part-timers-job-market-unlikely-to-return-to-former/

4 http://www.businessinsider.com/r-analysis-for-fed-a-muddled-jobs-report-even-as-us-employment-continues-to-expand-2015-7

5 S&P 500 performance between 3/9/09 and 5/1/2015 (Accessed July 5, 2015)

6 http://www.businessinsider.com/closing-bell-june-29-2015-6

7 https://www.frbatlanta.org/cqer/research/gdpnow.aspx (Accessed July 5, 2015)